In fintech, your API isn't just a technical interface it's the front door to your business, the backbone of your partnerships, and a prime target for regulators and attackers alike. A single misstep in your API design or security can lead to catastrophic data breaches, regulatory fines, or a complete loss of partner trust.

That's why "moving fast and breaking things" doesn't cut it here. You need to move fast and build unbreakable things. This requires more than just good developers; it requires API Governance a deliberate framework of policies, standards, and controls that ensures every API you build is secure, compliant, and reliable.

If you're leading a fintech team in the highly regulated US market, getting governance right isn't optional; it's existential. This checklist is your roadmap.

Now, let's build your fortress.

Why API Governance Matters So Much in US Fintech

Before jumping into the checklist, it’s worth understanding why governance is especially critical for fintech teams in the US.

Fintech APIs Sit at the Intersection of Risk and Scale

Fintech APIs often handle:

- Financial transactions

- Personally identifiable information (PII)

- Authentication and authorization data

- Integrations with banks, payment processors, and regulators

That means even small API decisions can have outsized consequences.

US Regulatory Pressure Raises the Bar

US fintech teams must consider:

- Data protection and privacy expectations

- Auditability and traceability

- Internal security policies

- External compliance requirements

Strong API governance helps you prove control, not just claim it.

What Is API Governance (In Plain English)?

API governance is the set of rules, processes, and tools that ensure your APIs are:

- Designed consistently

- Secure by default

- Easy to understand

- Safe to change

- Auditable over time

In short, governance helps teams move fast without breaking trust.

Why Governance is Non-Negotiable for US Fintech

The US financial landscape is a minefield of regulations: GLBA, FFIEC guidelines, NYDFS Cybersecurity Regulation (23 NYCRR 500), SEC rules, and state-level laws like the California Consumer Privacy Act (CCPA). Your APIs are directly in scope.

Beyond compliance, consider:

- Partner Trust: Banks and large institutions will conduct rigorous due diligence on your API security before integration.

- Developer Experience: Inconsistent APIs slow down your own teams and frustrate external developers.

- Business Risk: An API outage or breach can halt transactions, triggering contractual penalties and reputational damage that's hard to recover from.

Governance turns this risk into a competitive advantage: it makes your platform more trustworthy, easier to use, and safer to scale.

The Complete Fintech API Governance Checklist

Use this as a living document. Audit against it quarterly.

Category 1: Security & Authentication

1.1 Authentication & Authorization:

- Enforce Strong, Standardized Auth: Mandate OAuth 2.0 with PKCE for customer-facing apps. Use mutual TLS (mTLS) for highest-value B2B connections. Ban API keys in URL parameters.

- Implement Fine-Grained Authorization: Use a consistent model (e.g., RBAC, ABAC) across all APIs. Never rely on "front-door-only" checks; validate permissions at the endpoint level.

- Mandate Token Management: Enforce short-lived access tokens (minutes/hours) with secure refresh token rotation. Implement token binding.

1.2 Data Protection & Encryption:

- Encrypt Everything in Transit: TLS 1.2+ (mandate 1.3) is non-negotiable. Enforce strict cipher suites.

- Classify and Protect Data at Rest: Identify all PII (Personally Identifiable Information), PCI data, and non-public financial info. Ensure encryption per FFIEC and state laws.

- Mask Sensitive Data in Logs & Responses: Never log full account numbers, SSNs, or API keys. Use consistent masking patterns (e.g.,

XXX-XX-1234).

1.3 Threat Protection:

- Implement Rigorous Input Validation & Sanitization: Treat all input as malicious. Use strong, allow-list validation schemas (JSON Schema, OpenAPI).

- Enforce API Rate Limiting & Throttling: Define limits based on user tiers and endpoint risk. Implement graceful degradation, not just hard cuts.

- Deploy a Dedicated API Gateway/WAF: Use this layer for consistent policy enforcement (auth, rate limits), threat detection (OWASP Top 10 for APIs), and request/response transformation.

Category 2: Compliance & Regulatory Adherence

2.1 Audit Trails & Logging:

- Log All Access & Changes: Every API call must generate an immutable audit log with: timestamp, user/API client ID, endpoint, source IP, request/response identifiers, and outcome. This is critical for Reg SCI, SOC 2, and breach investigations.

- Maintain Data Lineage: For transactional APIs, implement trace IDs that follow a request across all microservices for full traceability.

- Secure and Retain Logs: Store logs in a secure, immutable system. Follow FFIEC-prescribed retention periods (often 3-7 years).

2.2 Data Privacy & Consent:

- Map Data Flows for CCPA/CPRA: Know what PII each API processes and where it flows. Build APIs to honor "Right to Delete" and "Right to Know" requests.

- Incorporate Consent Checks: For APIs handling consumer data, verify and record consent status before processing.

- Manage Third-Party Risk (Vendor APIs): Have a process to assess the security posture of any external API you integrate with. This is a direct requirement of NYDFS 500.

Category 3: Design & Development Standards

3.1 Consistency & Usability:

- Adopt an API-First Design Philosophy: Define the contract (OpenAPI Specification) before writing code. This aligns stakeholders and prevents drift.

- Standardize Naming, Errors, and Patterns:

- Use RESTful conventions or a clear GraphQL schema.

- Enforce a universal error response format (

{"code": "INSUFFICIENT_FUNDS", "message": "...", "traceId": "..."}). - Use ISO standards for dates, currencies, and country codes.

- Version All APIs: Use URL path versioning (

/api/v1/) or header versioning. Have a clear, documented deprecation policy (e.g., 12-month sunset period).

3.2 Documentation & Discoverability:

- Maintain Live, Interactive Documentation: Every API must have documentation that is always in sync with the running code. It should allow safe, sandboxed testing.

- Document Regulatory Impact: Tag endpoints in documentation with relevant compliance scope (e.g.,

[PCI-DSS],[GLBA]). - Publish a Public API Playbook: For external developers, provide clear guides on authentication, error handling, rate limits, and compliance requirements.

Category 4: Operational Excellence & Monitoring

4.1 Reliability & Performance:

- Define & Monitor SLOs/SLAs: Set Service Level Objectives for latency (p95, p99), throughput, and uptime (99.9%+). Monitor them religiously.

- Implement Comprehensive Health Checks: Have dedicated

/healthand/readyendpoints for all services, monitored by your orchestration platform. - Plan for Failure: Design for idempotency (critical for payments!) Implement circuit breakers and graceful fallbacks.

4.2 Change Management & Deployment:

- Enforce Code & Security Reviews: No API change merges without review. Use automated SAST/DAST tools in CI/CD.

- Maintain a Centralized API Registry: A single source of truth for all APIs, their owners, status, and contracts. This is vital for audits and partner inquiries.

- Use Canary/Blue-Green Deployments: Roll out API changes gradually to minimize blast radius.

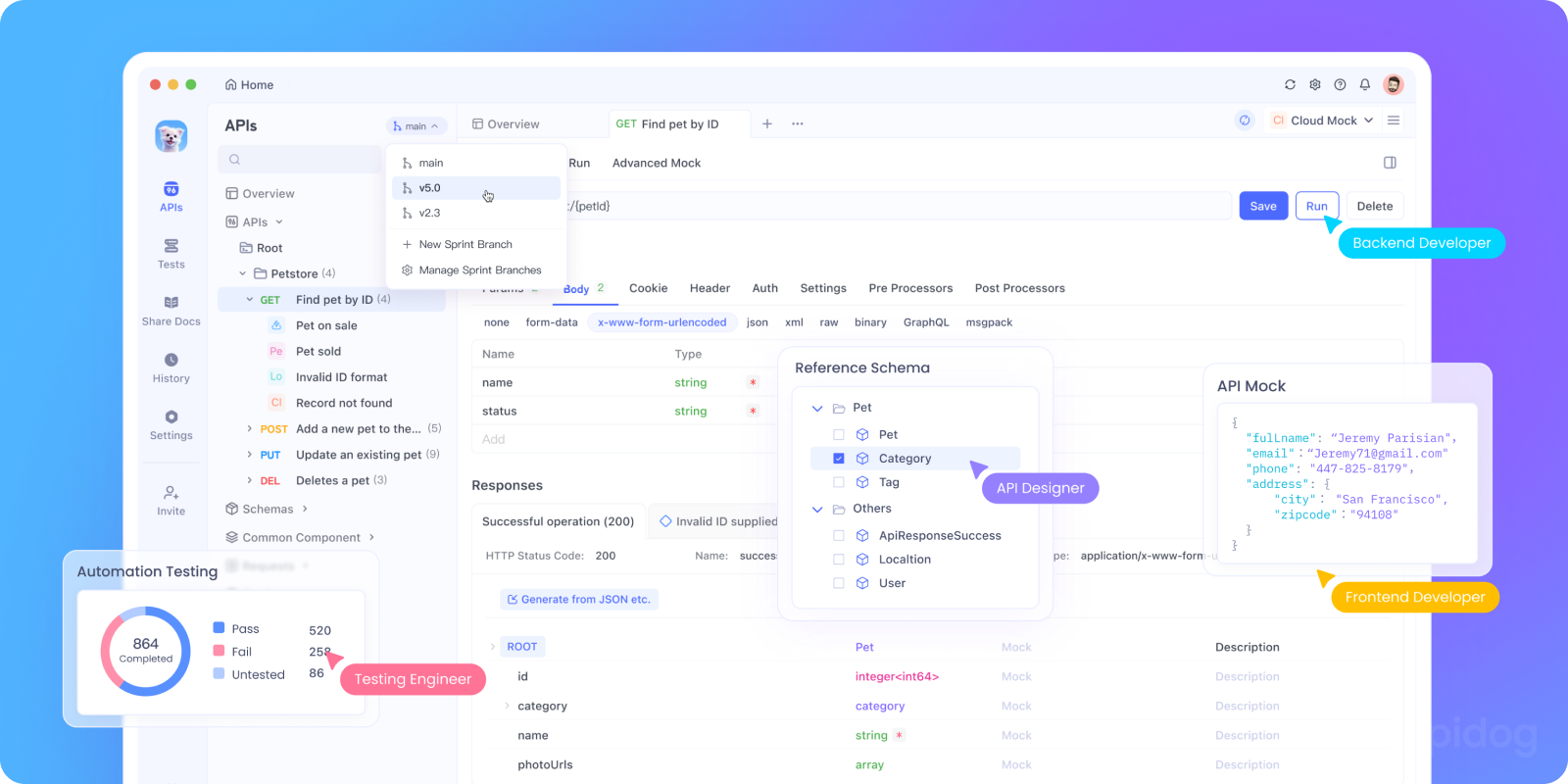

From Checklist to Reality: How Apidog Enables Fintech Governance

A checklist is just paper unless it's operationalized. This is where most teams struggle juggling disparate tools for design (Swagger), testing (Postman), mocking, documentation, and security reviews. The complexity creates gaps where governance fails.

Apidog is uniquely positioned as the central command center to enforce your governance framework. Here’s how it maps directly to the checklist:

- For Security & Design Standards: Apidog's design-first environment lets you define your OpenAPI spec with built-in validation. You can set team-wide style rules, mandate authentication schemes in the template, and generate mock servers instantly that adhere to the contract. This ensures consistency and security are baked in from the first whiteboard session.

- For Compliance & Documentation: Apidog automatically generates interactive, always-accurate documentation from your API designs. You can tag endpoints with compliance metadata. More importantly, every API test, mock, and real traffic can be logged and organized within Apidog, creating a searchable audit trail of how an API behaves and who tested what invaluable evidence for SOC 2 or security audits.

- For Operational Excellence: Apidog acts as your centralized API registry and collaboration hub. It provides a single pane of glass for developers, QA, and product managers to see all APIs, their versions, and their test statuses. Its powerful testing features allow you to build automated test suites that validate not just functionality, but also security policies (like rate limit behavior) and compliance requirements before deployment.

With Apidog, governance stops being a bottleneck and becomes an automated, integrated part of the development workflow. It’s the tool that helps you prove you’re following your own checklist.

Conclusion: Governance as Your Growth Engine

For US fintechs, robust API governance is the bedrock of sustainable growth. It’s what allows you to move at the speed of a startup while maintaining the trustworthiness of an incumbent bank. It turns your API platform from a potential liability into your most defensible asset.

This checklist provides the "what." A tool like Apidog provides the "how" turning governance principles from aspirational documents into automated, living practices embedded in your team's daily workflow.

Start building that foundation today. Your future partners, auditors, and customers will thank you for it.